The Psychology of Money: Master Behavioral Finance for Smarter Decisions

Introduction

Have you ever created a perfect budget, only to blow it on an impulse purchase? Or panic-sold stocks during a market dip, even though you knew you should hold for the long term? If so, you’re not alone. You’re simply human. Welcome to the fascinating, and often frustrating, world of the psychology of money.

The truth is, making smarter financial decisions has less to do with what you know and more to do with how you behave. Spreadsheets, data, and expert analysis are important, but they often crumble in the face of our own deeply ingrained cognitive biases and emotional responses. This is where behavioral finance comes in—a field that merges financial economics with psychology to explain why we make seemingly irrational choices with our money.

This guide will demystify the core principles of financial psychology. You’ll learn to identify the invisible scripts that dictate your financial behavior, understand the impact of emotions on money, and discover practical strategies to overcome these biases. By the end, you’ll be equipped to cultivate a resilient money mindset and build the financial discipline necessary for long-term financial success. It’s time to master your mind to master your money.

Why Your Brain is Bad at Money: The Clash of Emotion and Logic

Our brains are marvels of evolution, but they weren’t designed to navigate the complexities of the modern financial world. The part of our brain that managed immediate threats on the savanna—the fight-or-flight response—is the same part that reacts to a stock market crash. This creates a fundamental conflict between our emotional instincts and our rational goals.

This concept is often explained by Nobel laureate Daniel Kahneman’s “System 1” and “System 2” thinking.

- System 1: This is your fast, intuitive, and emotional brain. It makes snap judgments based on gut feelings and past experiences. It’s what makes you swerve to avoid a car or feel a jolt of panic when you see red numbers on your investment portfolio.

- System 2: This is your slow, deliberate, and analytical brain. It handles complex calculations, weighs pros and cons, and engages in long-term planning. It’s the part of you that builds a budget or researches an investment.

The problem? System 1 is almost always in the driver’s seat. It’s our default operating mode. When stress, fear, or excitement (greed) enters the financial equation, System 1 hijacks our decision-making process, often leading to choices that sabotage our System 2 plans. This is the heart of emotional investing and why understanding our human irrationality in finance is the first step toward better outcomes.

The goal isn’t to eliminate emotion—that’s impossible. The goal is to build systems and habits that allow our rational System 2 to stay in control, even when System 1 is screaming.

The Hidden Scripts: Unpacking the Most Common Financial Biases

Cognitive biases are systematic patterns of deviation from norm or rationality in judgment. In finance, these mental shortcuts are the primary drivers of bad money choices. By learning to spot them, you can start to neutralize their power over your wallet. Here are some of the most pervasive cognitive biases in finance.

H3: Overconfidence Bias: The “I Can Beat the Market” Trap

Overconfidence is the tendency to overestimate your knowledge, abilities, and the accuracy of your information. In investing, this often manifests as excessive trading, under-diversification, and taking on too much risk. You might believe you can pick the next big stock or time the market perfectly, despite overwhelming evidence that even seasoned professionals struggle to do so consistently.

- Example: An investor has a few successful stock picks and starts believing they have a special talent. They begin trading more frequently, ignoring diversification rules, and eventually suffer significant losses when their “hot streak” inevitably ends.

- The Fix: Acknowledge the role of luck in your successes. Stick to a well-researched, diversified, and long-term investment plan. Automation can be your best friend here. Related: AI Financial Assistants: Revolutionizing Personal Wealth can help you stick to a plan without emotional interference.

H3: Loss Aversion: Why Losing $100 Hurts More Than Gaining $100 Feels Good

Psychologically, the pain of a loss is about twice as powerful as the pleasure of an equivalent gain. This is loss aversion, and it’s a primary driver of poor investment decision making. It causes us to hold onto losing investments for far too long, hoping they’ll “come back,” while selling winning investments too early to “lock in” the gains.

- Example: You bought a stock at $50. It drops to $30. Instead of cutting your losses and reallocating the capital to a better opportunity, you hold on, thinking, “I’ll sell when it gets back to $50.” This is an emotional decision, not a financial one.

- The Fix: Evaluate your investments based on their future prospects, not their past performance or your purchase price. Ask yourself: “If I had this cash today, would I buy this stock?” If the answer is no, it might be time to sell.

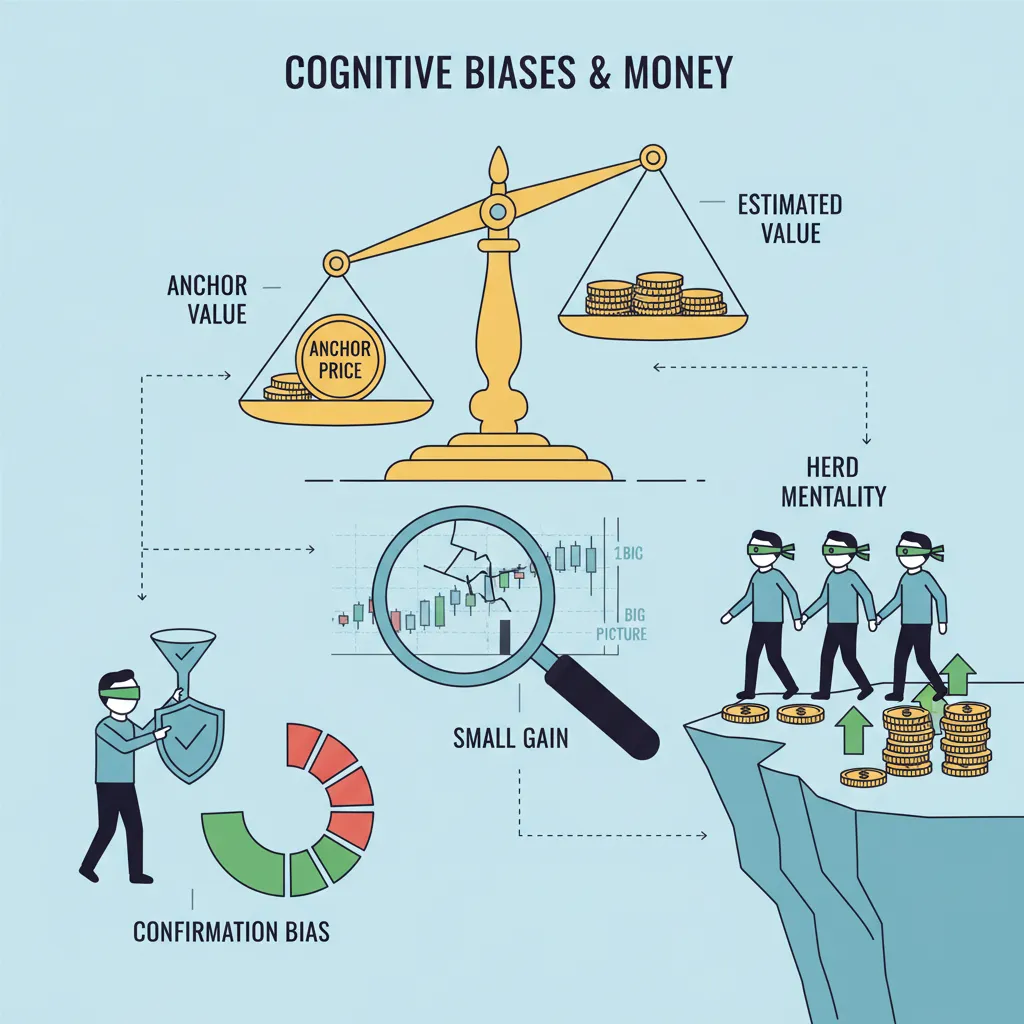

H3: Confirmation Bias: Seeing Only What You Want to See

Confirmation bias is the tendency to search for, interpret, favor, and recall information that confirms or supports your pre-existing beliefs. If you’re excited about a particular investment, you will subconsciously seek out articles, videos, and opinions that validate your decision, while dismissing or ignoring any negative information.

- Example: Before investing in a trendy tech company, you only read positive analyst reports and watch interviews with the enthusiastic CEO, while ignoring reports about the company’s high debt load and fierce competition.

- The Fix: Actively seek out dissenting opinions. Play devil’s advocate with your own ideas. Before making a significant financial move, make a genuine effort to understand the strongest arguments against it.

H3: Anchoring Bias: The First Number Always Sticks

Anchoring bias occurs when you rely too heavily on the first piece of information offered (the “anchor”) when making decisions. In finance, this could be the original price of a stock, the initial asking price of a house, or the first salary figure mentioned in a negotiation.

- Example: You see a stock that once traded at $200 and is now at $50. You anchor to the $200 price and think it’s a “bargain,” even if the company’s fundamentals have deteriorated and its true value is closer to $30.

- The Fix: Base your decisions on intrinsic value and current fundamentals, not on arbitrary past numbers. Conduct fresh research and analysis for every financial decision, ignoring irrelevant historical data points.

H3: Herding/Bandwagon Effect: Following the Crowd

Humans are social creatures, and this instinct spills over into our finances. The herding effect is the tendency to follow the actions of a larger group, regardless of your own independent analysis. This is fueled by the fear of missing out (FOMO) and the assumption that the crowd must know something you don’t. It’s a major factor in market bubbles and crashes.

- Example: Watching friends make huge profits on a meme stock or cryptocurrency and jumping in at the peak of the hype, only to see it crash shortly after.

- The Fix: Develop a solid financial plan and investment philosophy before you’re in the middle of a market frenzy. Write down your principles and stick to them. Remember that the point of maximum excitement is often the point of maximum risk.

Building a Resilient Money Mindset: From Theory to Practice

Understanding these biases is the first step, but true change comes from building new personal finance habits. Cultivating a strong money mindset is about creating a buffer between an emotional trigger and a financial action. It’s about shifting from reactive to proactive.

H3: The Power of Self-Awareness: Identify Your Financial Triggers

Begin by observing your own financial behavior without judgment. When do you feel most tempted to overspend? What market conditions make you feel fearful or greedy? Keep a financial journal for a month. Note not just what you spend, but how you felt when you spent it. Recognizing your patterns is crucial for overcoming financial biases.

H3: Develop a Strong Financial Plan (and Stick to It!)

A written financial plan is your most powerful tool against emotional decision-making. It’s a rational document created by your calm, logical System 2 brain. It should outline your goals, your savings rate, your investment strategy (including asset allocation and diversification), and your rules for buying and selling. When you feel panic or FOMO, refer back to your plan. It acts as a constitution for your financial life.

H3: Automate Your Good Habits for Financial Discipline

The easiest way to avoid bad money choices is to take your easily-distracted brain out of the equation. Automation is the key to building financial discipline.

- Automate Savings: Set up automatic transfers from your checking account to your savings and investment accounts the day you get paid. You can’t spend money you never see.

- Automate Investments: Use dollar-cost averaging by setting up regular, automatic investments into your chosen funds or ETFs. This removes the temptation to time the market.

- Automate Bill Payments: Avoid late fees and stress by automating all your recurring bills.

Related: AI Smart Home Automation: The Future of Connected Living shows how automation can simplify other areas of your life, and the same principles apply to your finances.

H3: Embrace a Long-Term Perspective

Wealth psychology is fundamentally about playing the long game. Compounding is the most powerful force in finance, but it only works over long periods. Tune out the daily noise of the market and focus on the decades ahead. One of the best ways to improve your risk tolerance psychology is to extend your time horizon. A 10% drop in the market feels like a disaster if you’re thinking about next week; it’s a minor blip on the radar if you’re thinking about the next 30 years.

Practical Strategies to Apply Behavioral Finance Today

Let’s move from mindset to direct action. Here are some simple, effective financial planning tips grounded in behavioral economics money principles that you can implement immediately.

H3: Use “Cooling-Off” Periods for Major Decisions

To combat impulsivity, implement a mandatory waiting period for any non-essential purchase over a certain amount (e.g., $100). The 24-hour or 72-hour rule works wonders. This allows the initial emotional excitement (System 1) to fade, giving your rational brain (System 2) a chance to evaluate the purchase properly.

H3: Reframe Your Perspective on Savings and Spending

The way you frame a financial choice dramatically affects your behavior.

- Save Money Psychology: Instead of thinking of saving as “depriving” yourself today, frame it as “paying” your future self. You are buying freedom, security, and options for the person you will be in 10, 20, or 30 years.

- Spend Money Psychology: When considering a purchase, don’t just think about its dollar cost. Translate it into “life energy” by calculating how many hours you had to work to earn that money. A $1,000 phone might feel different when you reframe it as 40 hours of your life.

H3: Create Financial “Guardrails” and Simple Rules

Simplify your decision-making by creating hard-and-fast rules. These guardrails prevent you from having to use willpower in the heat of the moment.

- “I will increase my 401(k) contribution by 1% every time I get a raise.”

- “I will not invest in any product I don’t fully understand.”

- “No more than 5% of my portfolio will be allocated to speculative assets.”

These rules are a core component of smart money management and financial decision science.

H3: Improve Your Financial Literacy Continuously

The more you understand the fundamentals of personal finance and investing, the less susceptible you will be to hype and fear. A strong knowledge base acts as an anchor for your System 2 brain, giving it the ammunition it needs to fight back against emotional impulses. Make a habit of reading reputable financial books, blogs, and news sources. Related: AI Tutors: Unlocking Student Potential with Adaptive Learning Paths highlights how new tools can accelerate learning in any field, including finance.

Conclusion: Mind Over Money

The journey to financial well-being is an internal one. It’s less about finding the perfect stock and more about understanding your own mind. The principles of behavioral finance and the psychology of money teach us that we are all predictably irrational. But in that predictability lies power.

By recognizing your cognitive biases, understanding your emotional triggers, and building robust systems to counteract them, you can bridge the gap between where you are and where you want to be. Start by automating your savings, writing down your financial plan, and implementing a cooling-off period for big purchases. These small behavioral changes, compounded over time, are what lead to true, lasting wealth and long-term financial success.

The ultimate goal is not to become a robot, devoid of emotion. It’s to create a financial life where your long-term goals are protected from your short-term impulses. What’s the one financial bias you recognize most in yourself? Take a moment to reflect, and then choose one strategy from this article to start implementing today. Your future self will thank you.

Frequently Asked Questions (FAQs)

H3: Q1. What is the main idea of the psychology of money?

The main idea is that our relationship with money and our financial success are driven more by our behavior, emotions, and psychological biases than by our intelligence or financial knowledge. It emphasizes that soft skills like patience, discipline, and managing expectations are often more critical than technical skills like financial modeling.

H3: Q2. What are the three main pillars of behavioral finance?

The three main pillars of behavioral finance are:

- Heuristics: People often make decisions based on mental shortcuts or rules of thumb, which can lead to errors.

- Framing: The way a problem or choice is presented (or “framed”) can significantly influence the decision an individual makes.

- Market Inefficiencies: Behavioral finance argues that psychological biases can lead to market anomalies and deviations from the efficient-market hypothesis, creating bubbles and crashes.

H3: Q3. How can I fix my money psychology?

You can improve your money psychology by first becoming aware of your own biases and emotional triggers through self-reflection. Then, create a structured financial plan to act as a rational guide. Automate your savings and investments to reduce impulsive decisions, adopt a long-term perspective, and implement simple rules or “guardrails” to guide your day-to-day financial behavior.

H3: Q4. What is the most common cognitive bias in finance?

While many biases are prevalent, overconfidence is arguably one of the most common and dangerous in finance. It leads investors to trade too frequently, underestimate risks, and fail to diversify their portfolios properly, often resulting in significant underperformance over the long run.

H3: Q5. How does emotional investing affect financial decisions?

Emotional investing, driven by fear and greed, causes investors to buy high (during market euphoria) and sell low (during market panic)—the exact opposite of a sound investment strategy. It leads to short-term, reactive decisions that sabotage long-term goals like retirement planning and wealth accumulation.

H3: Q6. What is the difference between behavioral finance and traditional finance?

Traditional finance assumes that people are rational economic agents who always act in their own self-interest and that markets are perfectly efficient. Behavioral finance, on the other hand, incorporates psychology to argue that people are often irrational, have predictable biases, and that these behaviors can lead to market inefficiencies and predictable patterns.

H3: Q7. What is a “money mindset”?

A money mindset refers to your underlying beliefs, attitudes, and feelings about money. It shapes how you earn, save, spend, and invest. A healthy or “growth” money mindset sees money as a tool for achieving goals and believes in the ability to improve one’s financial situation, while a “scarcity” mindset is often rooted in fear and the belief that financial resources are limited.