Master Your Money Abroad: The Ultimate Digital Nomad Finance Guide

Introduction

The allure of the digital nomad lifestyle is undeniable: the freedom to work from anywhere, explore diverse cultures, and craft a life unbound by traditional office walls. Yet, beneath the vibrant Instagram feeds and tales of exotic adventures lies a crucial, often underestimated, challenge: mastering your money abroad. For many, the transition from a single-country financial setup to a global one can feel like navigating a complex maze. Concerns about digital nomad finance, remote work financial planning, and managing money overseas quickly move from abstract concepts to daily realities.

This comprehensive guide is designed to empower you with the knowledge and tools to confidently handle your finances, no matter where your laptop takes you. We’ll delve into everything from choosing the best banks for remote workers and executing seamless international money transfers, to demystifying digital nomad taxes and crafting effective travel budget tips. Whether you’re a seasoned expat or just contemplating your first border-crossing workcation, understanding the nuances of global income streams and cross-border taxation is paramount. Our mission is to transform financial anxiety into financial freedom for digital nomads, ensuring your focus remains on your work and adventures, not on banking headaches or tax woes.

Let’s unlock the secrets to robust financial planning abroad and set you on the path to true financial independence as a digital nomad.

Setting Up Your Financial Foundation: Banking & Accounts

Establishing a solid financial base is the first and arguably most critical step for any digital nomad. Your banking setup needs to be as mobile and flexible as your lifestyle. Gone are the days when a single local bank account sufficed.

Choosing the Best Banks for Remote Workers

When you’re constantly on the move, traditional brick-and-mortar banks often fall short. They might impose foreign transaction fees, have limited international transfer options, or lack truly global customer support. This is where modern expat banking solutions come into play.

- Neobanks (Challenger Banks): These fully digital banks are often the top choice for digital nomads.

- Wise (formerly TransferWise): Renowned for its multi-currency account, which allows you to hold and convert money in over 50 currencies with real exchange rates and minimal fees. Its debit card is excellent for spending abroad.

- Revolut: Offers a similar multi-currency account, budget management tools, and sometimes even cryptocurrency features. They provide different tiers of accounts, including free and premium options with varied benefits.

- N26: Popular in Europe, N26 provides a fully mobile banking experience with low or no foreign transaction fees and robust security features.

- Starling Bank (UK-based): Offers fee-free spending abroad and excellent customer service, making it a favorite among UK digital nomads.

- Traditional Banks with Strong International Divisions: Some larger traditional banks have specialized international services or accounts designed for expats. While they might still have physical branches, their online platforms are usually robust.

- Consider banks with a global presence or partnerships that facilitate easy international money transfers and provide multi-currency support. Check their fee structures carefully.

Key Features to Look For:

- Multi-currency accounts: Essential for holding different currencies without constant conversion.

- Low or no foreign transaction fees: A major money-saver.

- Competitive exchange rates: Always aim for the real interbank rate or close to it.

- Easy international transfers: Fast, low-cost transfers to and from various countries.

- Robust mobile app: For managing your finances on the go.

- Excellent customer support: Available 24/7 and ideally through multiple channels (chat, email, phone).

- Debit card with global acceptance: Visa or Mastercard are usually best.

Essential Online Banking for Expats

Once you’ve chosen your primary banking partners, online banking for expats becomes your daily financial hub. Ensure your chosen platforms offer:

- Secure access: Two-factor authentication (2FA), biometric login, and strong encryption are non-negotiable.

- Bill payment capabilities: The ability to pay bills in different countries or currencies if needed.

- Spending analytics: Tools that help you track your expenditures and stick to your travel budget tips.

- Virtual cards: For secure online purchases, especially when using public Wi-Fi.

Prioritizing secure online finance is crucial. Always use a VPN on public Wi-Fi, be wary of phishing attempts, and regularly monitor your account activity. [Related: Master Your Day: 10 AI Tools to Skyrocket Your Personal Productivity]

Navigating the Global Money Maze: Transfers & Currency

Moving money across borders is a fundamental part of the digital nomad experience. Understanding how to do it efficiently, affordably, and securely can save you significant time and money.

International Money Transfer Strategies

Whether you’re sending money to family, paying for services, or receiving payments from clients, choosing the right platform for international money transfer is key.

- Dedicated Transfer Services:

- Wise (formerly TransferWise): Still a front-runner for its transparent fees and mid-market exchange rates. Ideal for regular, smaller transfers.

- Remitly & WorldRemit: Excellent for sending money to specific countries, often with various payout options (bank deposit, cash pickup, mobile money).

- Xoom (a PayPal service): Good for convenience, especially if you already use PayPal, but watch out for exchange rates and fees, which can sometimes be higher.

- Bank Transfers: Traditional bank wires can be reliable but are often slower and more expensive, especially for smaller amounts, due to correspondent bank fees and less favorable exchange rates.

- Peer-to-Peer (P2P) Apps: For informal transfers between friends or small payments, apps like PayPal or Venmo (US only) can work, but beware of international transfer fees and currency conversion rates.

Always compare fees and exchange rates across several services before initiating a transfer. Even a small difference can add up significantly over time.

Smart Currency Exchange Tips

Dealing with multiple currencies is a daily reality for digital nomads. Smart strategies can help you maximize your purchasing power and avoid unnecessary losses from poor currency exchange tips.

- Avoid Airport & Hotel Exchange Kiosks: Their rates are notoriously bad.

- Use Debit Cards from Neobanks: Cards from Wise, Revolut, or N26 typically offer near interbank exchange rates and often have fee-free ATM withdrawals up to a certain limit.

- “Decline Conversion” at ATMs: When using an ATM abroad, if it asks whether you want to be charged in the local currency or your home currency, always choose the local currency. This lets your bank (which usually offers a better rate) handle the conversion. This is known as Dynamic Currency Conversion (DCC) and is almost always more expensive.

- Carry Some Local Cash: While cards are widely accepted, having a small amount of local currency is always a good idea for small vendors, markets, or emergencies.

- Monitor Exchange Rates: Use apps like XE Currency Converter to track rates and understand when might be a good time to convert larger sums if you have that flexibility.

Cryptocurrency for Nomads

The rise of digital assets has introduced a new dimension to cryptocurrency for nomads. While volatile, crypto can offer certain advantages for cross-border transactions and wealth management.

- Faster, Cheaper Transfers: For large international transfers, stablecoins (cryptocurrencies pegged to fiat currencies like USDT or USDC) can be transferred quickly and at lower costs than traditional wire transfers, bypassing banking hours and traditional financial systems.

- Inflation Hedge: In countries experiencing high inflation, holding a portion of assets in stablecoins or major cryptocurrencies like Bitcoin can sometimes act as a hedge against local currency devaluation.

- Decentralized Finance (DeFi): Offers opportunities for earning interest on holdings, borrowing, and other financial services without traditional intermediaries, though this comes with higher risk and complexity.

Considerations:

- Volatility: Most cryptocurrencies are highly volatile, making them risky for short-term savings. Stablecoins mitigate this risk but are not entirely without their own.

- Regulatory Uncertainty: Regulations vary wildly by country, and some places have outright bans or strict rules on crypto.

- Security: Self-custody of crypto requires significant technical knowledge and vigilance against hacks and scams. Using reputable exchanges is crucial.

Cryptocurrency isn’t a replacement for traditional banking for most nomads but can be a powerful tool when understood and used strategically, particularly for global income strategies.

Mastering Your Money While on the Move: Budgeting & Saving

Life as a digital nomad comes with fluctuating expenses and varied income streams. Effective budgeting and consistent saving are the bedrock of long-term financial stability.

Crafting a Realistic Travel Budget

A clear budget is your roadmap to financial control. It helps you understand your spending, identify areas for savings, and avoid running out of funds unexpectedly.

- Track Everything: Use apps like YNAB (You Need A Budget), Mint, or Expensify to categorize and track every dollar (or peso, baht, euro) spent. This is the cornerstone of budgeting while traveling.

- Distinguish Fixed vs. Variable Costs:

- Fixed: Subscriptions (Netflix, Adobe), insurance, loan payments, some accommodation (if booked long-term).

- Variable: Food, transportation, entertainment, tours, spontaneous purchases. These are your biggest areas for control.

- Research Cost of Living Abroad: Before moving to a new destination, research its cost of living abroad. Websites like Numbeo or Expatistan provide excellent data on average prices for rent, food, transport, and leisure.

- Allocate “Discovery” Funds: Always budget a small amount for unexpected experiences or emergencies. The digital nomad lifestyle often presents unique opportunities that aren’t easily planned.

- Categorize and Review: Regularly review your budget (weekly or monthly) to see where your money is actually going versus where you planned for it to go. Adjust as needed.

Person budgeting on tablet in foreign cafe

Person budgeting on tablet in foreign cafe

Example Travel Budget (Monthly):

- Accommodation: $600 - $1200 (hostels to apartments)

- Food & Groceries: $300 - $600 (eating out vs. cooking)

- Transportation: $50 - $200 (local transport, occasional flights)

- Activities & Entertainment: $100 - $300

- Travel Insurance: $40 - $100

- Communication (SIM, internet): $20 - $50

- Miscellaneous/Buffer: $100 - $300

These travel budget tips are crucial for maintaining your digital nomad lifestyle cost and preventing financial surprises.

Saving as a Digital Nomad

Building an emergency fund and saving for future goals becomes even more critical when you don’t have a fixed address or traditional safety nets.

- Automate Savings: Set up automatic transfers from your primary checking account to a separate savings account (ideally a high-yield one) immediately after you get paid. “Pay yourself first” is a golden rule.

- Emergency Fund: Aim for 3-6 months of living expenses saved in an easily accessible, separate account. This is your safety net for unexpected medical issues, travel disruptions, or dips in income.

- Specific Savings Goals: Have dedicated savings goals for things like a new laptop, a big trip, a down payment on property, or retirement. Naming these accounts can increase motivation.

- Utilize High-Yield Savings Accounts (HYSAs): Even if your primary bank doesn’t offer a great rate, consider opening an HYSA with an online-only bank. Your money can still grow while being readily accessible.

- Be Mindful of Currency Fluctuations: If you’re saving in a foreign currency, be aware of its stability and potential for devaluation against your primary income currency. Diversifying savings across stable currencies can be a smart move.

Effective saving as a digital nomad is not just about accumulating wealth; it’s about creating financial resilience that supports your independent lifestyle.

The Tax Labyrinth: Digital Nomad Taxes & Residency

Taxes are arguably the most complex and anxiety-inducing aspect of financial planning abroad for digital nomads. The absence of a fixed residence can blur the lines of tax obligations, making proper planning essential to avoid costly mistakes.

Understanding Digital Nomad Taxes

There’s no single “digital nomad tax” system. Your tax obligations are a complex interplay of your nationality, where you earn your money, where you physically spend your time, and tax treaties between countries.

- Citizenship-Based Taxation: Countries like the USA tax their citizens on worldwide income, regardless of where they live. If you’re a US citizen, you’ll need to report your income to the IRS, though you might qualify for exclusions like the Foreign Earned Income Exclusion (FEIE) or foreign tax credits.

- Residency-Based Taxation: Most other countries tax individuals based on their tax residency. This means if you are deemed a tax resident of a country, you’ll typically pay taxes on your worldwide income there.

- Source-Based Taxation: Some countries tax income derived from sources within their borders, even if you are not a resident. For example, if you rent out property in a country you no longer reside in, that rental income might still be taxable there.

Navigating these rules requires an understanding of international tax advice and potentially consulting with a tax professional specializing in cross-border taxation.

Demystifying Tax Residency for Nomads

Tax residency is not the same as legal residency or citizenship. It’s a legal status determined by a country’s tax laws, primarily based on how much time you spend there and your ties to that country.

- Physical Presence Test: Many countries use a “183-day rule” – if you spend more than 183 days in a single tax year in one country, you’re often considered a tax resident. However, this is a simplification, and other factors apply.

- Center of Vital Interests: This is a more subjective test, looking at where your family lives, where your primary economic ties are (bank accounts, investments), and where you maintain social connections.

- Tax Treaties: These bilateral agreements between countries prevent double taxation. They contain “tie-breaker rules” to determine which country has the primary right to tax you if you could be considered a resident of both.

The goal for many digital nomads is to avoid becoming a tax resident in any high-tax country, often by strategically moving between locations to avoid triggering residency rules in any single place, or by establishing tax residency for nomads in a low-tax or no-tax jurisdiction. This strategy requires meticulous record-keeping of your travel dates and professional guidance.

Simplified digital interface for international tax management

Simplified digital interface for international tax management

Global Income Strategies and Compliance

Beyond understanding the rules, having a strategy for your global income strategies is crucial.

- Record Keeping: Keep meticulous records of all income (invoices, payment receipts), expenses, and travel dates (flight tickets, passport stamps). This is your primary defense in case of an audit.

- Professional Advice: Engage an international tax specialist or a firm that understands cross-border taxation and digital nomad taxes. This investment can save you significant money and stress in the long run.

- Business Structure: Consider the optimal legal structure for your business (e.g., sole proprietorship, LLC, offshore company). This can have significant tax implications depending on your home country and where you derive income.

- Utilize Tax Optimization Strategies: If eligible, make the most of foreign earned income exclusions, foreign tax credits, and other deductions available in your home country.

- Stay Informed: Tax laws change. Regularly check updates from tax authorities and professional bodies relevant to your citizenship and business structure. [Related: The AI Revolution: How Artificial Intelligence is Transforming Healthcare]

Building Wealth Abroad: Investing & Financial Freedom

Living abroad doesn’t mean putting your long-term financial goals on hold. In fact, for many digital nomads, the lifestyle offers unique opportunities to accelerate their journey toward financial freedom digital nomad status.

Investing for Nomads

While the idea of investing for nomads might seem daunting with constantly changing addresses, it’s entirely achievable with the right strategy and platforms.

- Brokerage Accounts for Non-Residents: Many traditional brokers have restrictions on clients who don’t reside in their home country. Look for international online brokerages that cater to expats and non-residents, such as Interactive Brokers, Charles Schwab International, or Saxo Bank.

- Diversification is Key: Don’t put all your eggs in one basket. Diversify across asset classes (stocks, bonds, ETFs, real estate), geographies, and currencies.

- Low-Cost Index Funds & ETFs: These are often the simplest and most effective way to invest. They provide broad market exposure, are cost-efficient, and require minimal active management.

- Robo-Advisors: Services like Betterment or Wealthfront (though primarily US-focused) offer automated investment management based on your risk tolerance. Look for international equivalents or services that accept non-US clients.

- Real Estate: While direct property ownership can be complex due to residency laws, consider indirect investments like REITs (Real Estate Investment Trusts) or crowdfunding platforms if you’re interested in real estate exposure.

- Factor in Currency Risk: If your investments are denominated in a different currency than your primary income or future expenses, be aware of currency fluctuations impacting your returns.

The goal is to set up a robust, diversified portfolio that aligns with your long-term goals and helps you achieve financial independence remote.

Achieving Financial Freedom as a Digital Nomad

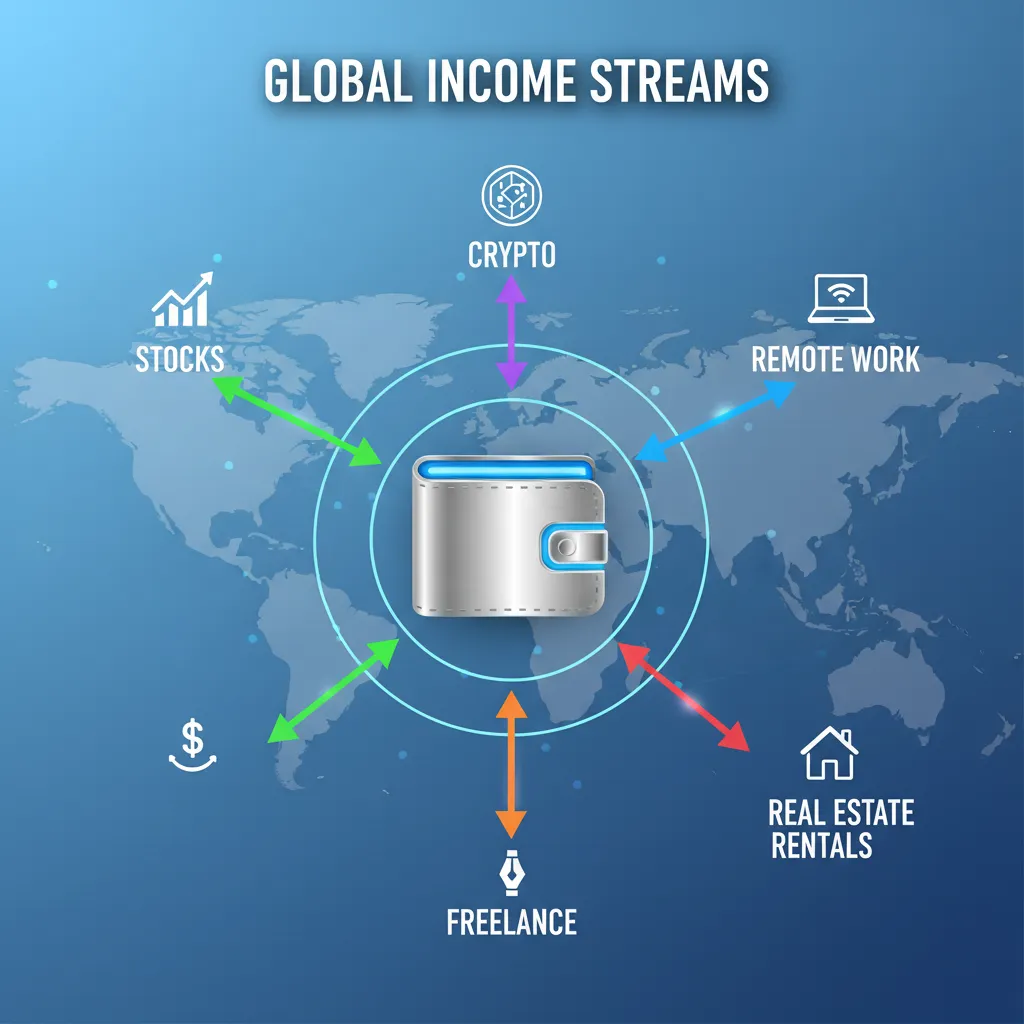

Financial freedom digital nomad isn’t just a dream; it’s an achievable goal through strategic income generation and smart wealth building.

- Multiple Income Streams: Relying on a single client or income source can be risky. Develop diverse income streams: freelance work, online courses, affiliate marketing, e-commerce, software as a service (SaaS), or a combination. This provides a buffer against economic downturns or client losses.

- Automate & Delegate: Focus on high-value work and automate repetitive tasks or delegate to virtual assistants. This frees up your time to explore new income opportunities or simply enjoy life.

- Passive Income: Actively work towards building passive income streams that don’t require your direct, daily involvement. This could include royalties from digital products, rental income, or dividends from investments.

- Geographic Arbitrage: Take advantage of the differing cost of living abroad. Earn in a high-currency country (e.g., USD, EUR) and live in a country with a lower cost of living (e.g., Southeast Asia, Latin America) to dramatically increase your savings rate and accelerate wealth accumulation.

Infographic showing global income streams and digital wallet

Infographic showing global income streams and digital wallet

Wealth Management for Nomads

As your wealth grows, wealth management for nomads becomes increasingly important. This involves more than just investing; it encompasses a holistic view of your financial health.

- Financial Advisor: Consider working with a financial advisor who specializes in cross-border wealth management and understands the unique challenges of digital nomads. They can help with tax-efficient investment strategies, retirement planning, and estate planning across multiple jurisdictions.

- Estate Planning: This is often overlooked but vital. What happens to your assets if something happens to you? You’ll need wills that are valid in relevant jurisdictions, and potentially trusts, especially if you have assets in multiple countries.

- Retirement Planning: Traditional retirement accounts might not be accessible or optimal for nomads. Explore international SIPP (Self-Invested Personal Pension) options, global brokerage accounts for long-term investments, or even property investments as part of your retirement strategy.

- Currency Hedging: For significant wealth, consider strategies to hedge against adverse currency movements, especially if you have liabilities or future expenses in a different currency than your primary assets.

Proper financial planning abroad for wealth management ensures your hard-earned money continues to grow and is protected for your future, wherever you are. [Related: Top AI Tools for Creativity & Productivity in 2024]

Protecting Your Nomad Life: Insurance & Security

While the freedom of the digital nomad lifestyle is exhilarating, it also comes with unique risks. Robust insurance coverage and stringent security practices are non-negotiable for peace of mind and financial protection.

Essential Digital Nomad Insurance

Traditional insurance policies are often designed for residents of a single country and may not provide adequate coverage for those constantly on the move. Digital nomad insurance is specifically tailored to your mobile lifestyle.

- Health Insurance: This is paramount.

- Travel Medical Insurance: Short-term policies designed for specific trips, covering emergencies, accidents, and some medical treatments abroad. Companies like SafetyWing, World Nomads, and Heymondo are popular choices.

- International Health Insurance: Comprehensive, long-term policies that cover routine medical care, specialist visits, and often include options for repatriation. These are more akin to traditional health insurance but with global coverage. Cigna Global, Aetna International are examples.

- Evacuation Insurance: Crucial for remote areas, ensuring you can be transported to a facility that can provide appropriate medical care if needed.

- Travel Insurance: Covers trip cancellations, delays, lost luggage, and personal liability. Often combined with travel medical insurance.

- Contents/Gadget Insurance: Protects your valuable electronics (laptops, cameras, phones) against theft, loss, or damage – essential for your mobile office.

- Liability Insurance: Provides coverage if you accidentally cause injury to another person or damage to their property. Some health or travel policies include a limited form of this.

- Business Liability/Professional Indemnity: If you run a business, ensure you have appropriate coverage for your professional services, especially if you work with international clients.

Always read policy details carefully, understand what’s covered (and what’s not), and be aware of geographical limitations or exclusions.

Secure Online Finance Practices

Your digital life is your livelihood. Protecting your online finances from cyber threats is as important as physical security. These secure online finance tips should be part of your daily routine.

- Strong, Unique Passwords: Use a password manager (e.g., LastPass, 1Password) to generate and store complex, unique passwords for every online account.

- Two-Factor Authentication (2FA/MFA): Enable 2FA on all financial accounts, email, and critical online services. Hardware keys (YubiKey) offer the strongest protection, followed by authenticator apps (Google Authenticator, Authy). Avoid SMS-based 2FA as it’s less secure.

- Use a VPN (Virtual Private Network): Always use a reputable VPN when connecting to public Wi-Fi networks in cafes, airports, or hotels. This encrypts your internet traffic, protecting your data from potential eavesdroppers.

- Regular Software Updates: Keep your operating system, browser, and all applications updated. Updates often include critical security patches.

- Cloud Backup: Regularly back up all important documents, photos, and work files to a secure cloud service (Google Drive, Dropbox, OneDrive) or an external hard drive. This protects you against device loss or theft.

- Be Wary of Phishing & Scams: Always double-check sender email addresses and links before clicking. Banks and legitimate services will rarely ask for sensitive information via email or unsolicited calls.

- Review Financial Statements: Regularly check your bank and credit card statements for any unauthorized transactions. Report suspicious activity immediately.

Hand holding passport with investment app on phone and world map

Hand holding passport with investment app on phone and world map

Advanced Tools & Resources for the Modern Nomad

The financial landscape for digital nomads is constantly evolving, with new technologies and services emerging to simplify global money management. Leveraging these remote finance tools can give you a significant advantage.

Remote Finance Tools & Apps

Beyond banking apps, several specialized tools can enhance your financial management.

- Budgeting & Expense Tracking:

- YNAB (You Need A Budget): A powerful budgeting app based on the “zero-based budgeting” philosophy, highly recommended for its ability to give every dollar a job.

- Mint: A free app that connects to your bank accounts to track spending and categorize transactions automatically.

- Expensify: Great for scanning receipts and automating expense reports, particularly useful if you have business expenses.

- Invoicing & Accounting:

- FreshBooks / Wave Accounting / Xero: Cloud-based accounting software that allows you to send invoices, track payments, manage expenses, and generate financial reports from anywhere. Essential for freelancers and small business owners.

- Tax Preparation & Filing:

- Tax software: For US citizens, services like TurboTax or H&R Block may have expat versions. For more complex situations, international tax software or specialists are advised.

- Multi-Currency Wallets:

- Beyond Wise and Revolut, explore other digital wallets that support various currencies and offer easy payment options.

- VPN Services:

- NordVPN, ExpressVPN, Surfshark: Reputable VPN providers crucial for online security.

These tools streamline your financial planning abroad and free up time for your work and adventures. [Related: Boosting Productivity: Top AI Tools Revolutionizing Workflows & Creativity]

The Future of Remote Finance

The landscape of remote finance is continually being shaped by technological advancements, with AI and blockchain leading the charge.

- AI-Powered Financial Assistants: Expect more sophisticated AI tools that not only track spending but offer personalized financial advice, optimize investments based on market trends, and even proactively flag potential tax issues based on your travel patterns.

- Blockchain & DeFi Expansion: Beyond simple crypto transfers, decentralized finance (DeFi) platforms are likely to offer more user-friendly and regulated services for lending, borrowing, and yield farming, creating new avenues for wealth management for nomads.

- Hyper-Personalized Financial Products: As data analysis improves, banks and fintech companies will offer highly customized products and services specifically designed for the unique needs of digital nomads, including dynamic insurance policies and flexible credit solutions.

- Global Digital Identities: The development of secure, verifiable digital identities could simplify KYC (Know Your Customer) processes, making it easier to open accounts or access services in new countries without extensive paperwork.

- Seamless Cross-Border Payments: Expect even faster, cheaper, and more integrated solutions for international money transfers, blurring the lines between domestic and international transactions.

The future of remote finance promises an even more streamlined, intelligent, and interconnected financial ecosystem for the global workforce. [Related: The Future is Now: AI Revolutionizing Personalized Learning & Education]

Conclusion

The digital nomad lifestyle offers unparalleled freedom, but true liberation comes with financial mastery. From the moment you contemplate your first international move, understanding digital nomad finance becomes your passport to sustained success. We’ve explored the essentials: from choosing the right expat banking solutions and executing seamless international money transfers, to demystifying digital nomad taxes and building wealth through smart investing for nomads.

By diligently applying travel budget tips, leveraging cutting-edge remote finance tools, and prioritizing secure online finance, you can transform potential financial anxieties into powerful growth opportunities. Embrace the challenge of financial planning abroad as an integral part of your adventure. With a proactive approach, continuous learning, and perhaps a little professional guidance, you can achieve genuine financial freedom digital nomad style, ensuring your journey is as prosperous as it is adventurous.

So, pack your bags, fire up your laptop, and embark on your global adventure with the confidence that your finances are as mobile and resilient as you are. The world is waiting, and your well-managed money is ready to explore it with you.

FAQs

Q1. What is the best bank for digital nomads?

There isn’t a single “best” bank, as needs vary. However, neobanks like Wise, Revolut, and N26 are highly recommended for digital nomads due to their multi-currency accounts, low fees, excellent exchange rates, and user-friendly mobile apps. They are designed for international use.

Q2. How do digital nomads handle taxes while traveling?

Digital nomads handle taxes based on their citizenship and tax residency. US citizens are taxed on worldwide income but may qualify for the Foreign Earned Income Exclusion (FEIE). Most other nationalities are taxed based on where they establish tax residency, often determined by the 183-day rule or their “center of vital interests.” Consulting an international tax specialist is crucial.

Q3. How can digital nomads send and receive money internationally without high fees?

Digital nomads primarily use dedicated international money transfer services like Wise (formerly TransferWise), Remitly, or WorldRemit, which offer competitive exchange rates and lower fees than traditional bank wires. For business, invoicing platforms often integrate payment solutions.

Q4. Is travel insurance enough for digital nomads, or do I need health insurance?

Travel insurance typically covers medical emergencies and trip-related issues for short periods. For long-term digital nomad living, a comprehensive international health insurance policy (e.g., from SafetyWing or Cigna Global) is highly recommended. These provide broader coverage, including routine medical care, beyond just emergencies.

Q5. How can I budget effectively as a digital nomad with fluctuating income?

Effective budgeting for digital nomads involves tracking all expenses rigorously using apps like YNAB or Mint, researching the cost of living in new locations, separating fixed from variable costs, and building a generous emergency fund. The “zero-based budgeting” method is particularly useful for fluctuating income.

Q6. Can digital nomads invest while living in different countries?

Yes, digital nomads can invest, but it requires careful planning. You’ll need to find international online brokerages (like Interactive Brokers or Charles Schwab International) that accept clients from various countries, as many traditional brokers have residency restrictions. Diversifying investments across asset classes and geographies is key.

Q7. What is “geographic arbitrage” for digital nomads?

Geographic arbitrage is a strategy where digital nomads earn income in a high-value currency (e.g., USD, EUR) but choose to live in countries where the cost of living is significantly lower. This allows them to save more money, invest more aggressively, and achieve financial independence faster than if they lived in a high-cost area.